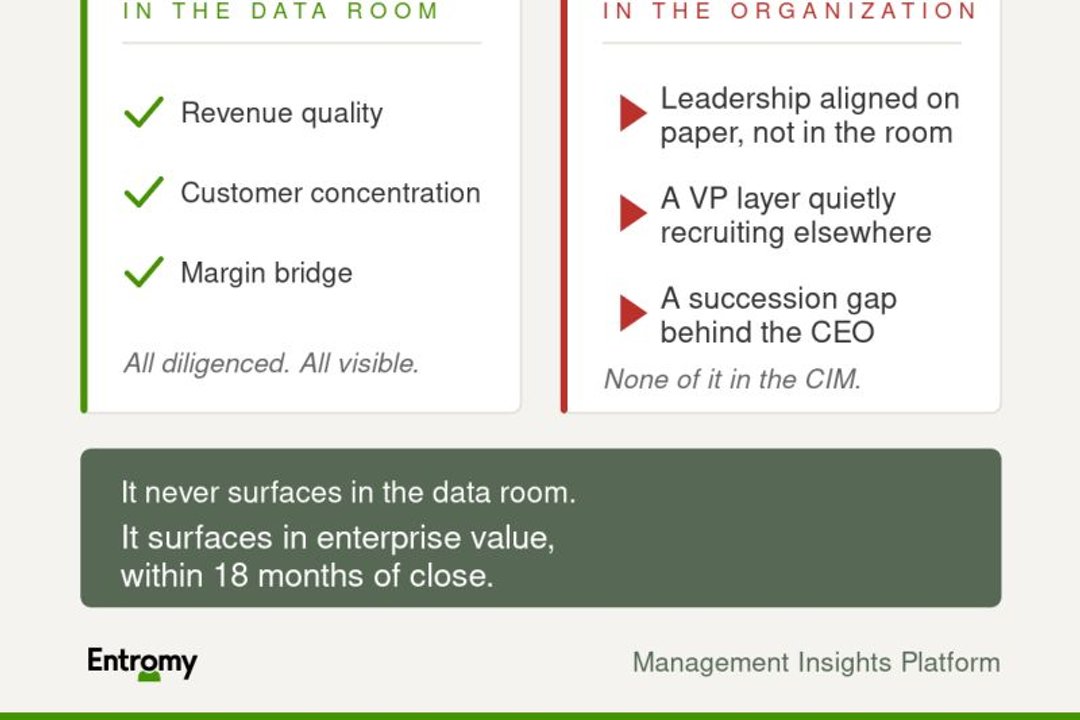

Three weeks before exclusivity, a deal team had the model buttoned up. Revenue quality, customer concentration, margin bridge, all diligenced to the decimal. Nobody had looked at the organization. That is the norm, not the exception. Organizational due diligence usually starts after close, once the firm already owns the outcome. By then the work is not de-risking a decision. It is managing one that has already been made.

A few weeks earlier, on a different deal, a team member put the habit into words. He had spent eleven years mostly doing software deals and told me: "We usually gloss over the employee stuff. It's a software business." Now his team was a few weeks from exclusivity on a 200-person professional services firm, and the old playbook did not quite fit. In software, you underwrite recurring revenue and 80% gross margins. In a services firm, you underwrite the people. The instinct to skip the org read did not update fast enough for the asset in front of him.

Why organizational due diligence lands after close

Financial, commercial, and legal diligence get weeks of specialist attention before exclusivity because the tools and the access exist to do it fast. Organizational due diligence gets skipped for none of the reasons deal teams usually cite when asked, and all of the reasons that actually hold up under pressure.

Access is genuinely constrained pre-close. You cannot run town halls or interview forty managers before signing. Confidentiality rules the process, and any read of the organization has to work within that constraint rather than against it. So teams default to what is available: management presentations, reference calls with people the seller hand-picked, and the CEO's own account of the team underneath them. None of that is an organizational read. It is a curated narrative.

Habit does the rest of the work. Most diligence playbooks were built around the businesses that dominated deal flow for the last decade, where the product scales independent of the people running it. A services firm, a healthcare platform, a business with a high-touch delivery model does not follow that model. The team member's own words apply generally: the instinct to gloss over "the employee stuff" survives long after the deal type has changed underneath it.

Until recently, there was no fast way to do it. An engagement survey takes months to field, requires internal access a seller will not grant before signing, and produces a mood reading rather than a structural one. Without a way to get a rigorous organizational read inside a live process, "we'll figure it out post-close" was not laziness. It was the only option on the table.

What a pre-close organizational read actually looks like

The shift is not adding more diligence. It is doing organizational diligence with the same discipline already applied to the financials, inside the same window.

A pre-exclusivity org read has to work with the access a live deal actually allows: leadership interviews structured against the thesis, targeted reference conversations, and where the process permits it, a confidential organizational assessment of the layer below the C-suite. The goal is not comprehensive coverage. It is a structural view of the same questions the model already assumes answers to. Does the leadership team have the bench strength to execute the plan. Where does the organization's confidence in the thesis diverge from the seller's narrative. Which capability gaps are cosmetic and which are load-bearing.

This is where org health diligence differs from a satisfaction check. It is not asking whether people are happy. It is asking whether the organization, as structured and staffed today, can deliver the specific value creation plan the deal team is underwriting. That is a different question, and it is the one that belongs in the same room as the margin bridge.

What changes when you de-risk instead of manage

An organizational read done before exclusivity changes the shape of the decision, not just its timing. It gives the deal team a basis to adjust price, structure earnouts around retention risk, or walk from a deal where the numbers work but the leadership bench does not exist to execute the plan. None of that is available once the deal has closed. Post-close, the same finding becomes a remediation project instead of a negotiating point, and the firm is spending its own capital and time fixing something it could have priced in.

There is a second, quieter benefit. A firm that shows up with a credible organizational read before close starts the relationship with management differently than one that shows up to "assess the team" three months into ownership. The first conversation is diligence. The second one, done for the first time after the deal is signed, reads as suspicion. Firms that get this right treat the pre-close read as the first step of a longer arc, one that continues into the 100-day baseline once the deal closes and the value creation plan needs a shared, factual starting point.

Practical guidance for deal teams

Build the organizational read into the diligence workstream list from the start of exclusivity discussions, not as a side request once the model is done. Treat it with the same seriousness as a quality of earnings report: a defined scope, a specific set of questions tied to the thesis, and a deadline that fits the process.

Scale the question to the asset. For a business where the product or the platform carries the value, a lighter organizational check may be enough. For a people-intensive business, professional services, healthcare delivery, anything where the org chart is close to the balance sheet, the organizational read deserves the same weight as customer concentration analysis. The team member who spent eleven years underwriting software deals was not wrong about software. He was applying a software answer to a people question.

Bring operating partners into the read early rather than after signing. They are the ones who will live with whatever the deal team assumed about the organization, and their pattern recognition across the portfolio is exactly what a single deal team, looking at one asset for the first time, does not have. Firms running this discipline across the platform, not just deal by deal, are the ones for whom organizational diligence for PE firms becomes infrastructure rather than a one-off ask.

And once the deal closes, do not let the pre-close read sit in a drawer. Carry it into the first 100 days, track the same questions with execution pulse monitoring, and treat the initial read as the first data point in an ongoing conversation with the organization rather than a diligence artifact that served its purpose at signing. The firms that treat organizational rigor as a discipline rather than a checkbox are the ones for whom the case for Entromy is really about what happens before the wire transfer, not just after it.

Nobody sets out to buy a business without understanding who runs it. But that is what happens every time the org read starts after close. The fix is not more diligence. It is the diligence that already exists for everything else, applied to the organization, on the same clock as everything else.

This article expands on a LinkedIn post by Jan Jamrich, CEO of Entromy.