A few weeks ago I sat in on an op review I've seen play out a hundred times before. OKR updates on the screen, numbers underwhelming for what the CEO admitted, unprompted, was the n'th quarter in a row. Nobody in the room was surprised. That was the part that stayed with me. If the miss wasn't a surprise to the people closest to it, then the stall had been forming for a while before it ever showed up on this slide.

That is the question worth sitting with. By the time an execution stall reaches your financials, how many quarters has it actually been forming underneath them? I support op and business reviews across dozens of PE-backed management teams and their operating sponsors, and the pattern is consistent enough that I no longer treat it as a coincidence. The financials are a lagging confirmation of something the organization already knew.

The wrong question is the one everyone asks

Most portfolio op reviews run on the same question: are we on track against plan? It feels rigorous. It has a scorecard, a set of milestones, a red-yellow-green. But it is fundamentally a backward-looking question. It pulls the room's attention to what recorded history shows, quarter-end actuals, board-deck metrics, the KPIs that were locked in at close. By the time those numbers are bad enough to trigger concern, the underlying execution problem is already several quarters old. You are diagnosing a symptom that took its time to surface.

Across roughly twenty-five recent engagements, I have watched this same dynamic repeat. The review process is doing its job on paper. Everyone can point to the tracker and say where the company stands against the plan. What the tracker cannot tell you is why the next quarter is going to disappoint, because that answer does not live in last quarter's numbers. It lives with the people running the plan on the ground.

The right question looks forward

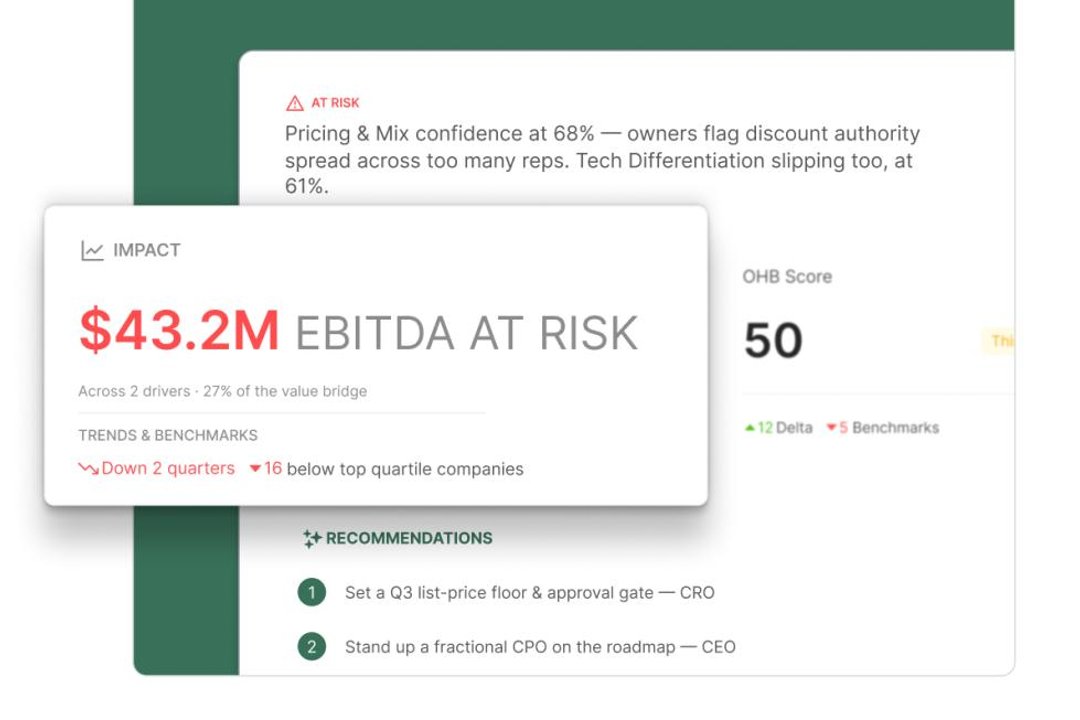

The question that actually protects the investment is different: what do the people executing the value creation plan have to say about the risk of a stall next quarter, and what are the top three things they see forming right now? That is not a rhetorical reframe. It changes who you're listening to and when. Instead of interrogating a spreadsheet after the quarter closes, you're asking the sales director, the plant manager, the regional VP, the people with a direct line of sight to customers and frontline execution, what they are seeing before it becomes a variance.

This is the difference between a rearview mirror and a windshield. The value creation plan sets the destination and the milestones, but the people closest to the work know earliest when a milestone is starting to slip, and usually why. An account team that is quietly losing renewal conversations, a plant that is running short-staffed heading into a demand spike, a product team that has stopped believing in a roadmap commitment: none of that shows up in the trailing financials for one or two quarters. It shows up in what people say when you ask them directly and consistently.

What forward-leaning CEOs actually do

The best portfolio company CEOs I work with do not wait for a retrospective report to tell them what already happened. They stay oriented toward what is about to happen. In practice that means treating the voices of the people executing the plan, the ones talking to customers and running operations in real time, as a primary input rather than an occasional temperature check. It is a habit, not a project. They build a continuous line into the organization instead of reconstructing one after a bad quarter forces the question.

That habit looks different from the legacy approach of an annual engagement survey mailed out once a year and reviewed months later. A survey cadence like that cannot catch a stall while it is still forming, because by the time the results are compiled, the quarter it was measuring is already over. What forward-leaning CEOs use instead is closer to continuous sensing: a standing, structured organizational pulse on how the plan is actually landing with the people responsible for it, refreshed often enough to catch a shift while there is still time to act on it. They treat that read the way they treat pipeline data or working capital: something you check regularly because it moves, not something you audit once a year.

The partner who consistently hits plan

Across roughly sixty PE firm clients I have worked with this past year, there is a pattern worth naming directly: at nearly every firm, there is at least one operating partner whose companies consistently hit plan. It is not luck, and it is not that their portfolio happens to draw easier theses. It is that they know about the execution problem before it becomes an execution miss. That is proactive stewardship, not superior forecasting.

What separates that partner from the rest of the operating team usually comes down to sequencing. They are not waiting for the board deck to raise the flag. They have built a habit, with the CEOs they back, of checking in on execution risk on a cadence that runs ahead of the reporting cycle, not behind it. When a stall starts forming, they hear about it from the org while it is still a fixable operating issue, not from a KPI dashboard after it has become a written-down thesis.

This is a structural advantage available to any operating partner working across a portfolio, not a personality trait. It requires treating the org itself as a source of forward-looking signal, alongside the financial and operational metrics that already get reviewed every quarter. For portfolio companies executing against an aggressive value creation plan, that means the review question in every op meeting should include, explicitly, what the frontline is seeing coming, not only what the ledger already recorded.

Cheap to fix while it is still small

The value of catching a stall early is not abstract. An execution problem caught while it is still an operating conversation, a resourcing gap, a customer relationship going sideways, a team losing confidence in a roadmap commitment, is inexpensive to correct. The same problem, left to mature for two or three quarters until it shows up in the financials, has usually compounded: lost customers, missed hiring windows, a leadership team now defending a miss instead of preventing one. The gap between those two costs is the entire case for continuous sensing over retrospective reporting.

The op reviews that work are the ones that stop asking only what already happened and start asking what the organization sees coming. That single shift, in the question asked and the frequency it's asked at, is what turns a review from a report card into an early warning system. The financials will tell you about the stall eventually. The people running the plan already know.

This article expands on a LinkedIn post by Brad Smith, Ph.D.